after the latest results")

€33.33: This is how much analysts estimate the value of Fastned BV (AMS:FAST) after the latest results

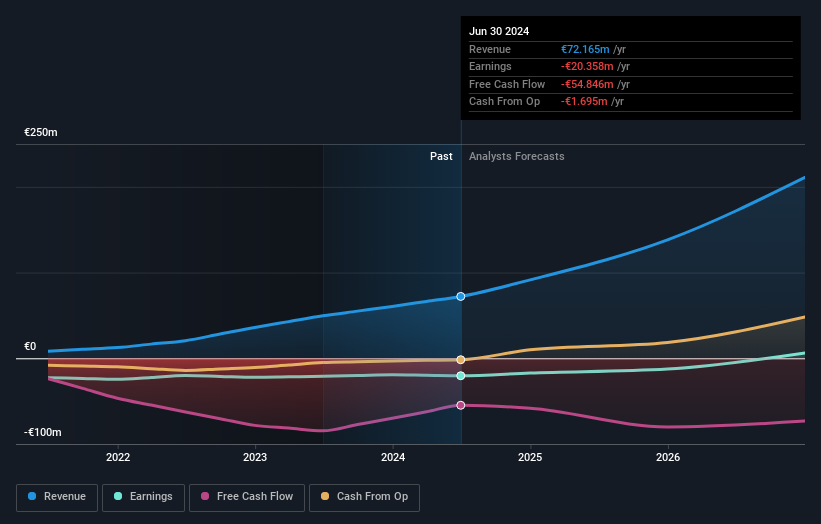

Investors in Fastned BV (AMS:FAST) had a good week as its shares rose 9.7% to close at €17.62 following the release of its half-year results. Revenues were €38m, with Fastned BV coming in around 3.1% below analyst expectations. This is an important time for investors as they can follow a company’s performance in its report, look at what experts are forecasting for next year, and see if expectations for the company have changed. We thought readers would find it interesting to see the latest analysts’ (statutory) forecasts for next year following the earnings announcement.

Check out our latest analysis for Fastned BV

Following the latest results, Fastned BV’s nine analysts are now forecasting revenues of €91.5 million in 2024. This would be a notable 27% increase in revenue compared to the last 12 months. Losses are expected to decline, shrinking 14% year-on-year to €0.92. Before this latest report, the consensus had expected revenues of €93.7 million and a loss of €0.84 per share. So it’s pretty clear that the consensus is more negative on Fastned BV after the new consensus numbers; while the analysts reduced their revenue estimates, they also made a moderate increase in loss per share expectations.

The consensus price target fell 7.7% to €33.33 as analysts are clearly concerned about the company following the weaker revenue and earnings outlook. The consensus price target is simply an average of individual analysts’ targets, so it might be helpful to see how wide the range of underlying estimates is. Currently, the most optimistic analyst values Fastned BV at €45.00 per share, while the most pessimistic analyst values it at €22.00. This is a fairly wide range of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the company.

These estimates are interesting, but it can be useful to draw the forecasts a bit more roughly when comparing them with Fastned BV’s past performance and with competitors in the same industry. From the latest estimates, we can conclude that the forecasts expect a continuation of Fastned BV’s historical trends, as the 61% annual revenue growth until the end of 2024 is roughly in line with the 55% annual growth over the past five years. In contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue by 6.5% per year. So, while Fastned BV is expected to maintain its revenue growth rate, it is definitely expected to grow faster than the industry as a whole.

The conclusion

Most importantly, analysts have raised their loss per share estimates for next year. They have also lowered revenue estimates for Fastned BV, but industry data suggests the company is expected to grow faster than the wider industry. The consensus price target has dropped significantly as analysts seem not to have been reassured by the recent results, leading to a lower estimate of Fastned BV’s future valuation.

With this in mind, we still believe that the long-term development of the company is much more important for investors. We have estimates – from several Fastned BV analysts – out to 2026, and you can see them for free here on our platform.

You can check for free here on our platform whether Fastned BV has too much debt and whether its balance sheet is healthy.

New: AI Stock Screeners and Alerts

Our new AI Stock Screener scans the market daily to uncover opportunities.

• Dividend powerhouses (3%+ yield)

• Undervalued small caps with insider purchases

• Fast-growing technology and AI companies

Or create your own from over 50 metrics.

Try it now for free

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.