to your portfolio now")

Reasons to add Leonardo DRS (DRS) to your portfolio now

Leonardo DRS, Inc. With a strong backlog and rising earnings expectations, DRS offers a great investment opportunity in the Zacks Aerospace sector.

Let’s focus on the factors that make this Zacks Rank #2 (Buy) company a strong investment choice right now.

Growth forecasts and surprise story

The Zacks Consensus Estimate for DRS’s earnings per share (EPS) for 2024 has increased 3.7% to 84 cents over the past 60 days. The Zacks Consensus Estimate for Leonardo DRS’s total revenue for 2024 is $3.15 billion, representing year-over-year growth of 11.4%.

The company’s long-term (three to five years) earnings growth is 16.4%. Over the last four quarters, it delivered an average earnings surprise of 25.60%.

Debt level

Leonardo DRS’s TIE was 8.3 at the end of the second quarter of 2024, above its peer group’s TIE ratio of 5.51. The company’s strong TIE ratio suggests that it can easily meet its interest payment obligations in the near future.

Currently, Leonardo DRS’s total debt ratio is 13.42%, which is significantly better than the industry average of 59.28%.

liquidity

The company’s liquidity ratio was 2.01 at the end of the second quarter of 2024, above the industry average of 1.79. The ratio, which is greater than one, shows that Leonardo DRS is able to meet its future short-term liabilities without difficulty.

Growing gap

DRS’s total backlog increased a solid 81.9% year-over-year to $7.93 billion as of June 30, 2024. The acceptance of a multi-boat contract to support electric propulsion activities in the Columbia-class submarine program with the U.S. Navy was the primary driver of the backlog increase. Such solid backlog growth indicates strong revenue growth prospects for the company in the coming quarters.

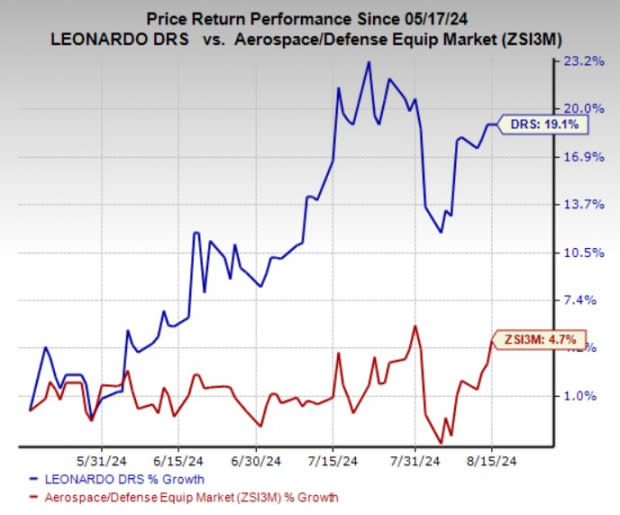

Price-performance

Over the past three months, DRS shares have seen a 19.1 percent rally compared to industry growth of 4.7 percent.

Image source: Zacks Investment Research

Other stocks to consider

Some other high-ranking stocks from the same industry are Curtiss Wright Corp. CW, TransDigm Group Inc. TDG and BAE Systems BAESY, all of which currently have a Zacks Rank of 2. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Curtiss-Wright delivered an average earnings surprise of 11.52% over the trailing four quarters. The Zacks Consensus Estimate for CW’s total revenues for 2024 is $3.04 billion, representing growth of 6.9% from the reported 2023 figure.

TransDigm’s long-term earnings growth rate is 20%. The Zacks Consensus Estimate for TDG’s fiscal 2024 revenues is $7.86 billion, representing an improvement of 19.4% over reported fiscal 2023 revenues.

BAE Systems’ long-term earnings growth rate is 12.4%. The Zacks Consensus Estimate for BAESY’s 2024 revenues is $35.84 billion, representing an improvement of 36.3% over the reported 2023 revenues.

Want the latest recommendations from Zacks Investment Research? Download the 7 best stocks for the next 30 days today. Click here to get this free report

Transdigm Group Incorporated (TDG): Free Stock Analysis Report

Bae Systems PLC (BAESY): Free Stock Analysis Report

Curtiss-Wright Corporation (CW): Free Stock Analysis Report

Leonardo DRS, Inc. (DRS): Free Stock Analysis Report

To read this article on Zacks.com, click here.

Zacks Investment Research