")

Bridgestone: Pressure from cheap Thai imports in key markets (OTCMKTS:BRDCF)

sfe-co2

Bridgestone Corporation (OTCPK:BRDCF)(OTCPK:BRDCY) saw some pressure on some of its more profitable products as cheap Thai imports took the market by storm and inventory was reduced ahead of possible higher tariffs. While Bridgestone cheaper compared to our competitors, unlike in our previous reportingand are doing slightly better than some specialty segment rivals, they are still affected by the Thai import situation and could see another quarter of pressure before things improve more significantly. There are also industry-wide pressures on new vehicle demand that suggest a recession.

Latest results

The latest results are interesting and we will compare them with Michelin (OTCPK:MGDDF). First of all, the first half of the year looks quite good, but the pressure has increased for Bridgestone in the second quarter.

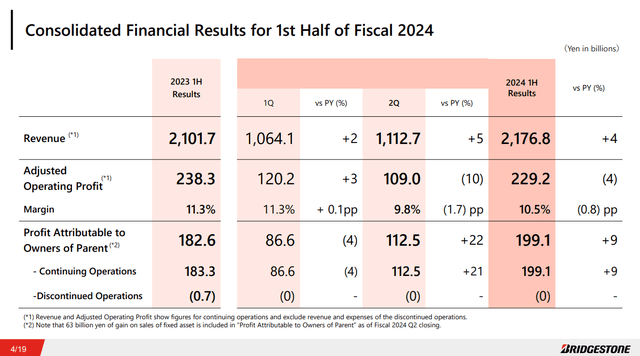

Headline results (H1 Press)

Volumes were under pressure but were comparatively in a decent position compared to competitors, but negative mix effects and general competitive pressure in the truck business led to significant margin losses in this business. Industrial debt and reductions in unit sales worsened the situation in operating profits. The Firestone brand for trucks and buses performed relatively weakly, as a lot of purchases were made in the US market in particular, where Bridgestone is more active than other tire offers outside the USAfrom cheap imports from Thailand, where many low-cost rubber products are manufactured because the raw materials are easy to obtain there. In addition, Expectation of tariffs on these imports, which has already begun with anti-dumping duties in the USA The supply shortages, which could become more permanent from October this year, led to even more extreme purchases of substitute products in the current quarters as retailers increased their inventories before the products became more expensive.

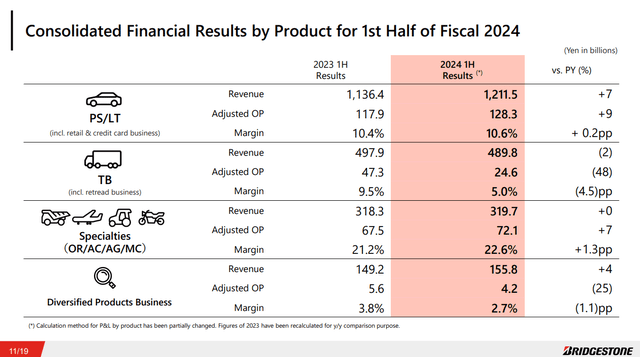

Segment results (H1 Press)

The specialty business recorded a fairly stable development, even in mining, where Michelin had to accept certain declines due to inventory reductions, the development was stable.

The general trends are rising prices for natural rubber, which is an inevitable raw material, and a general decline in demand for tires for new vehicles. The situation was particularly bad in Asia, which drove the trend for business in this region.

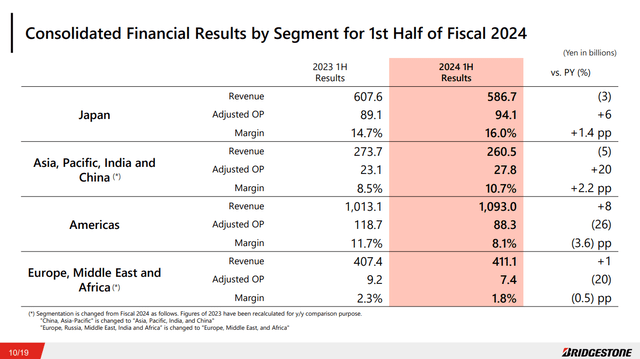

Geographies (H1 Press)

Latin American companies also suffered. While Argentina is struggling with austerity measures, Brazil, which is otherwise a strong consumer market, is also very competitive and is suffering from cheap imports from Thailand.

Conclusion

The company will generally address earnings pressure with further cost-cutting initiatives and offer products with higher margins and prices. Pressure from cheap imports is also expected to ease, probably starting next quarter, but at the latest after that, when panic buying stops. The problem is that this could trigger another wave of inventory reductions even if tariffs on these cheap imports are imposed in Bridgestone’s key markets. Ongoing macroeconomic pressures are also a concern, especially since the automotive industry has been in limbo for a long time, with pent-up demand in automotive markets still being consumed and production rates increasing only slowly since the semiconductor shortages.

In other words, we are not overweight the sector as macro pressures are becoming clear and high margin segments in some cases are starting to come under pressure year-on-year, including mining tires. In Bridgestone in particular, we note that while the P/E is now discounted slightly below 10% versus peers such as Michelin, the significant sales in the US and Latin America remain a disadvantage, although some Latin American markets have better prospects than the more developed markets. The potential de-inventory that could result from the imposition of tariffs clouds the picture in addition to the end market issues. All in all, not particularly compelling.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these securities.

If you found our perspective on this company interesting, you can also check out our Idea Room. The Value LabWe focus on long-only value ideas that are of interest to us, trying to find international mispriced stocks and Portfolio return of approx. 4%. We’ve done really well over the last 5 years, but we’ve also had to get our hands dirty in the international markets. If you’re a value investor who’s serious about protecting your wealth, our bunch could help broaden your horizons and give you some inspiration.